1. What is the North America Micro Mobile Data Center Market Overview – definition, scope, and significance?

The North America Micro Mobile Data Center market comprises self‑contained, transportable IT infrastructure solutions that deliver compute, storage, and networking capabilities in a compact, rack‑based format. These units range from sub‑25 RU modules to large, above‑40 RU systems and serve industries requiring rapid deployment, edge computing, or temporary capacity. Their significance lies in enabling low‑latency services, disaster recovery, and on‑site processing for sectors such as BFSI, healthcare, and manufacturing, thereby supporting digital transformation across the region.

2. What are the market drivers, restraints, challenges, and opportunities?

Key drivers include the surge in edge‑computing workloads, the need for rapid‑deployment data solutions in disaster‑prone areas, and increasing bandwidth demand from high‑density networks. Restraints stem from high upfront capital costs and regulatory compliance complexities in mobile deployments. Challenges involve integration with legacy IT environments and limited skilled personnel for field installations. Opportunities arise from the growth of 5G, IoT expansion, and government incentives for resilient infrastructure.

3. What are the current growth trends shaping the market?

Trend analysis shows a shift toward modular, scalable designs that allow customers to expand capacity by adding rack units. Vendors are integrating advanced cooling technologies and AI‑based monitoring to improve energy efficiency. Additionally, there is a rising preference for hybrid deployments that combine on‑premise micro data centers with public‑cloud services, especially in the high‑density network and remote office segments.

4. How has COVID‑19 impacted the market and what is the recovery trajectory?

The pandemic accelerated demand for remote‑office support and instant‑deployment data centers as organizations sought continuity amid lockdowns. Supply‑chain disruptions temporarily slowed production, but the need for resilient, off‑site compute resources spurred rapid adoption. Recovery is robust, with a clear upward trajectory as companies continue to invest in flexible infrastructure to mitigate future disruptions.

5. Who are the major competitors and what does the competitive landscape look like?

The market is populated by global technology leaders such as Dell Technologies Inc, Hewlett Packard Enterprise Development LP (HPE), Huawei Technologies, and Schneider Electric, alongside specialized providers like Canovate Electronics, Rittal GmbH & Co. KG, and VERTIV. Consolidation is moderate, with strategic partnerships and acquisitions focusing on expanding service portfolios and geographic reach, particularly in the large‑enterprise segment.

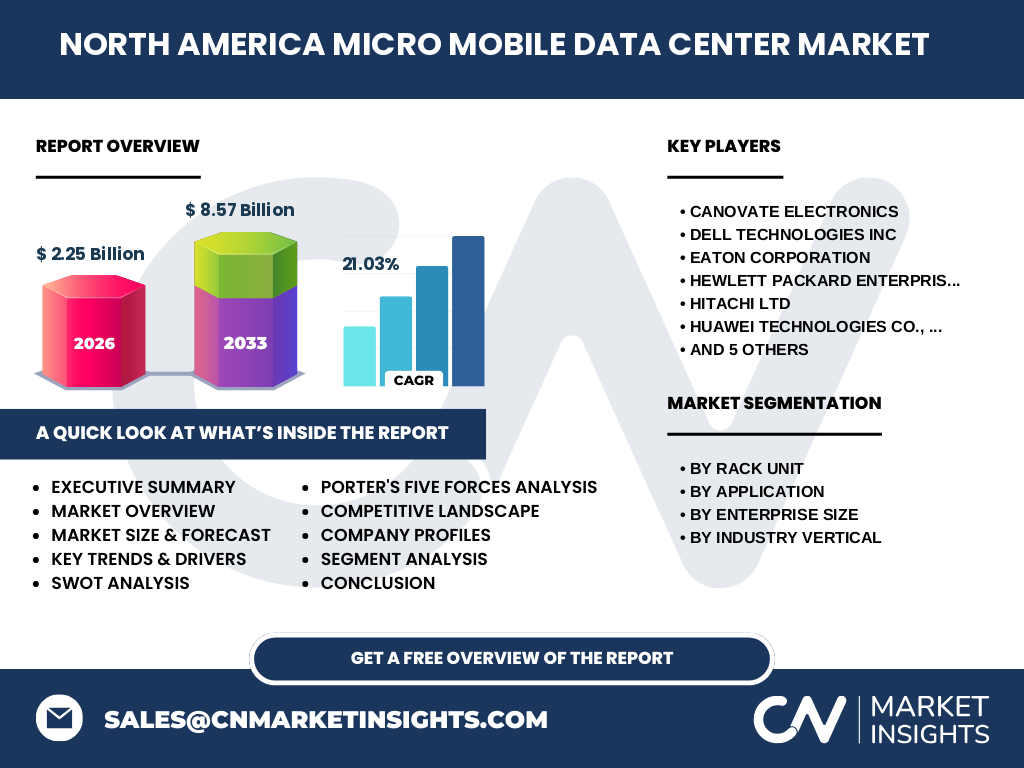

6. What are the key findings in the executive summary?

The North America Micro Mobile Data Center market is valued at USD 2.25 billion in 2026 and is projected to reach USD 8.57 billion by 2033, driven by a compound annual growth rate of 21.03 %. Growth is underpinned by high‑density network expansion, remote‑office demand, and the transition to edge‑centric architectures. Large enterprises dominate, while SMEs increasingly adopt modular solutions for cost‑effective scalability.

7. What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 21.03 %, the market is expected to maintain strong momentum, expanding from the 2026 baseline of USD 2.25 billion to well beyond the 2027‑2033 forecast of USD 8.57 billion. This trajectory indicates sustained investment in mobile data center technology across all segments, with particular acceleration in the 25‑40 RU and above‑40 RU rack unit categories.

8. How is the market sized and shared by segmentation?

By rack unit, the market is split among up to 25 RU, 25‑40 RU, and above 40 RU configurations, each catering to distinct capacity needs. Application segmentation includes instant DC & retrofit, high‑density networks, remote office support, and mobile computing, reflecting varied use cases. Enterprise‑size analysis shows large enterprises leading adoption, while SMEs are gaining traction in remote‑office and mobile‑computing applications. Industry verticals such as BFSI, retail, healthcare, IT & telecom, and manufacturing each command niche demand based on latency and compliance requirements.

9. What is the global North America market size and share by region?

Within the global context, North America holds a leading share of the micro mobile data center market, anchored by mature IT ecosystems and high investment capacity. While precise regional percentages are not disclosed, the region’s 2026 valuation of USD 2.25 billion underscores its position as the primary growth engine for the worldwide market.

10. What does the regional analysis reveal about market performance?

Performance varies across the United States, Canada, and Mexico. The United States drives the majority of demand due to extensive enterprise deployments and strong 5G rollout. Canada shows steady growth, particularly in healthcare and mining sectors that benefit from mobile compute. Mexico’s market is emerging, propelled by remote‑office projects and government initiatives to improve digital infrastructure.

11. Which companies lead the market and what are their strategies?

Key players include Dell Technologies, HPE, Huawei, and Schneider Electric, each leveraging broad product portfolios and global service networks. Dell focuses on integrated edge solutions, HPE emphasizes hybrid cloud interoperability, Huawei invests in AI‑enhanced management, and Schneider Electric prioritizes energy‑efficient designs. Smaller innovators such as Canovate Electronics and VERTIV differentiate through rapid customization and field services.

12. How does Porter’s Five Forces shape the market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of buyers is elevated as enterprises demand flexible pricing and rapid delivery. Bargaining power of suppliers remains low because component sourcing is diversified. Threat of substitutes is limited, with traditional fixed data centers unable to match mobility. Industry rivalry is intense, fostering innovation and strategic alliances.

13. What are the SWOT insights for the market?

Strengths: High scalability, rapid deployment, and support for edge workloads.

Weaknesses: Elevated initial cost and complexity of field integration.

Opportunities: Expansion of 5G, increasing remote‑work infrastructure, and government resilience programs.

Threats: Regulatory hurdles and competition from cloud‑native edge services.

14. How is value created along the market’s value chain?

The value chain starts with component manufacturing (servers, cooling, power modules), followed by system integration and ruggedization by OEMs. Next, logistics and field deployment services deliver units to customer sites. Ongoing value is generated through monitoring, maintenance, and upgrade services, often bundled as managed solutions to ensure uptime and performance.

15. What investment insights can be drawn from the market?

Investors should target companies with strong modular portfolios and proven field‑service capabilities. Partnerships that combine hardware expertise with software‑defined management platforms offer higher margins. The high CAGR suggests robust upside, especially in the above‑40 RU segment and high‑density network applications, making growth‑stage funding and strategic acquisitions attractive.

16. What are the concluding takeaways?

The North America Micro Mobile Data Center market is on a rapid growth trajectory, powered by edge computing, 5G rollout, and the need for resilient, mobile infrastructure. With a projected market size of USD 8.57 billion by 2033 and a 21.03 % CAGR, the sector presents substantial opportunities for vendors, investors, and end‑users seeking flexible, future‑proof data solutions.

17. How was the research conducted?

Research combined primary interviews with industry executives, secondary data from vendor reports, and quantitative modeling based on the provided market size and CAGR. Trend analysis incorporated technology roadmaps, regulatory reviews, and macro‑economic indicators relevant to North America.

18. What is the scope of the research?

The study covers the North American region, segmenting the market by rack unit size, application, enterprise size, and industry vertical. It excludes detailed financial breakdowns beyond the supplied figures and does not project market share percentages for individual companies.

19. Which key companies have recent developments in the market?

Recent announcements include Dell Technologies’ launch of a new AI‑optimized micro data center, HPE’s partnership with a major telecom carrier for edge deployments, Huawei’s rollout of 5G‑ready mobile units, and Schneider Electric’s introduction of an energy‑management module for remote sites. VERTIV reported a strategic acquisition of a field‑service provider, enhancing its deployment capabilities, while Canovate Electronics unveiled a fast‑assembly rack system targeting SMEs.